Historically, China has had a unique and turbulent relationship with Bitcoin.

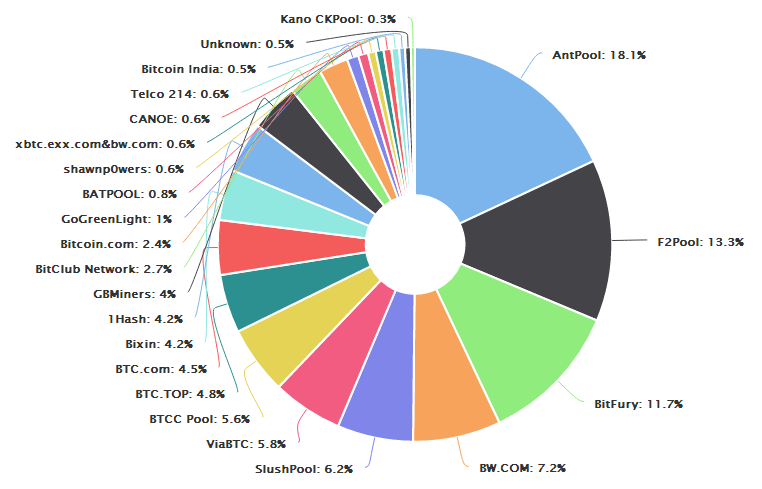

China is the world’s leading Bitcoin mining hub, generating at least 71% of the network hashrate according to a 2018 report. Some of the world’s largest crypto companies are Chinese, with multi-billion-dollar companies like Bitmain dominating the industry. With a flourishing OTC trade sector, the nation has long been a major source of demand on the Bitcoin network, with Chinese current events exerting major influence over the price action.

The country that plays such a major role in Bitcoin activity also has imposed some of the most stringent regulations and limitations on crypto trading in the world. China has effectively “banned” or restricted different aspects of Bitcoin and cryptocurrency trading several times over the years, denouncing Bitcoin as an unstable currency and even developing its own state-run cryptocurrency to take Bitcoin’s place. However, that’s not to say the current administration is anti-Bitcoin.

In this post, we’ll take a look at the nature of China’s relationship with Bitcoin and a timeline of major events since the launch of the world’s first cryptocurrency.

China’s Relationship to Bitcoin In the Last Decade

Some of the world’s largest Bitcoin companies have emerged from China despite the strict government stance on crypto assets. Here’s a brief recap of Bitcoin in China over the last 10 years.

- June 2009 — China bans the use of digital currencies to buy real-world goods and services to curtail video-game currencies subverting the yuan.

- June 2011 — Chinese bitcoin exchange BTCC is launched within a year of the first-ever crypto exchange.

- 2013 — Industry giants like Huobi and Bitmain are founded in China, going on to become the biggest crypto exchange and mining hardware manufacturer, respectively.

- May 2013 — Bitcoin receives nationwide media attention due to a fundraising event; Chinese interest in Bitcoin skyrockets.

- December 2013 — The Chinese government bans Bitcoin from banks and domestic exchanges.

- March 2014 — A false report circulates of an outright ban on all Bitcoin transactions in China. BTC price drops.

- August 2015 — Four Chinese mining pools (F2Pool, AntPool, BTCC Pool, and BW.com) account for half of the Bitcoin network’s hashrate.

- November 2016 — A weakened Chinese yuan leads to a surge in Chinese investment. BTC prices increase.

- September 2017 — China bans ICOs and domestic Bitcoin exchange activity, leading to an exodus of companies.

- January 2018 — A 65% crash in BTC price leads 90% of blockchain-focused VC firms in China to leave the market.

- October 2019 — President Xi Jinping stresses the importance of blockchain investment for China’s future.

- 2020 — The Chinese government is set to release its own state-run cryptocurrency, perhaps indicating that while blockchain is welcome, Bitcoin is less well regarded.

Below, we’ll dig into some of the big events in the timeline and how they shaped Bitcoin’s future.

Early 2013: Bitcoin Gains Nationwide Publicity in China

In 2013, Bitcoin had rarely made international headlines. What few news stories there were in the west were typically skeptical, discussing the high risk of Bitcoin or connecting it with the black market. This changed in China in April 2013 when a Chinese charity called One Foundation announced that it was accepting Bitcoin. This was at a time when Bitcoin was the only cryptocurrency in existence. Major charities accepting BTC would make industry news even today, and in 2013, such news was groundbreaking.

Private fundraising organizations fall under stringent regulations in China, and One Foundation started out as a subsidiary of the Health Ministry’s Red Cross Society of China. The Red Cross Society became embroiled with a corruption scandal, damaging its reputation and that of One Foundation by association. A major earthquake hit southwest China in 2013, and when the RCSC announced that it would inspect the affected area, it faced major backlash.

Tens of thousands of microbloggers voiced a lack of confidence in the organization’s integrity. RCSC efforts to raise funds for an earthquake that killed nearly 200 people and injured 15,500 yielded just $23,000. “As an ordinary citizen, I will never donate a penny to the Red Cross Society,” wrote one citizen on social media. One Foundation saw the lack of response and took a different tack, appealing to internet users by offering to accept bitcoins. The charity released a statement saying:

“Welcome geeks and hackers’ bitcoin donations to the One Foundation.”

The charity received 230 BTC, worth around $30,000, accounting for 1% of the total funds raised to help with earthquake relief. This event highlighted the interest of Chinese citizens in Bitcoin. State media released positive reports about One Foundation’s actions, likening Bitcoin to other digital, centralized currencies in China like Q-coin.

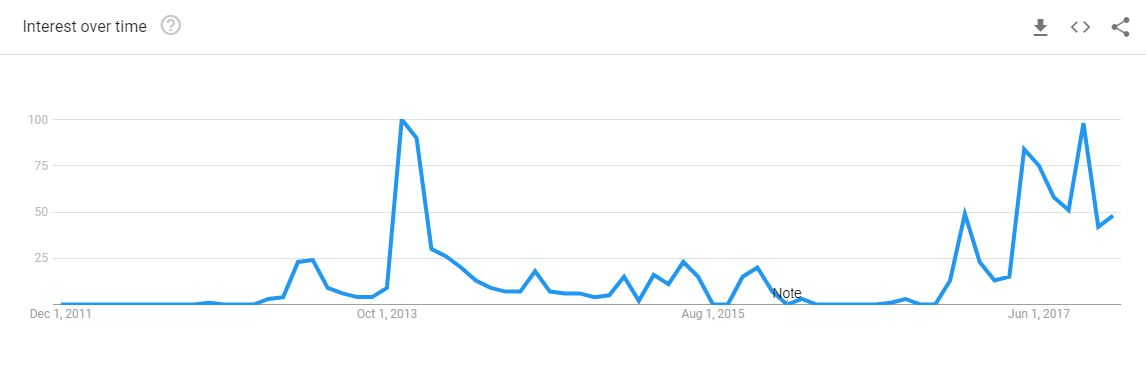

As evidenced by Chinese Google Trends data from that time, interest in Bitcoin surged following the news story.

Late 2013: Bitcoin Adoption Meets Bitcoin Regulation in China

2013 was a rough year for Bitcoin, with the collapse of the world’s leading Bitcoin exchange, Mt. Gox, looming on the horizon. At the same time, the Silk Road saga was unfolding: in October, the FBI shut down the dark web marketplace for good, seizing an amount of BTC worth around $4 million at the time.

However, despite some of the negative press Bitcoin was receiving, the fledgling cryptocurrency was becoming increasingly accepted by Chinese institutions. The Chinese state search engine, Baidu, began accepting Bitcoin. Taobao, the world’s largest e-commerce website, followed suit. Demand soared, and crypto exchange BTCChina went from being the largest in the nation to the largest in the world by volume, surpassing Mt. Gox.

Chinese interest in Bitcoin helped push prices from $50 to new record highs, seeing an 800% price increase in two months. With both the national search engine and the biggest e-commerce website around accepting Bitcoin payments, it seemed that the cryptocurrency was on a path toward legitimacy and widespread adoption. However, the sudden rise of the decentralized currency may have alarmed Chinese authorities, for they took action shortly thereafter.

On December 4, the Chinese central bank released a statement about Bitcoin saying that financial institutions “must not use bitcoin to set the price for products or services, not buy and sell bitcoins… and not directly or indirectly provide other bitcoin-related services including registering, trading, clearing or settlement.” The central bank declared that Bitcoin was not legal tender and thus could not be used in financial institutions.

Shortly afterward, Baidu and Taobao removed all references to bitcoin payments from their sites. Baidu released a statement blaming Bitcoin volatility for the decision to suspend the acceptance of Bitcoin; the next day, the price dropped 20%. This was a major event in the Bitcoin space.

The largest instances of Bitcoin adoption in China to date had just been undone, and the impact on the price as well as business development was severe. However, that didn’t stop what are now some of the world’s most prominent Bitcoin companies from flourishing.

Bitcoin’s Titans of Industry in China

2013 onward also marked the dawn of Chinese crypto giants. Bitmain, the world’s largest manufacturer of the specialized ASIC hardware used to mine Bitcoin, was founded in China in 2013. The founder, Jihan Wu, would go on to become a major player in the space as a leading supporter of the Bitcoin Cash hard fork in 2017. One of the largest BTC mining pools, Antpool, is owned by Bitmain, and some have argued that this gives Wu significant influence over the Bitcoin network.

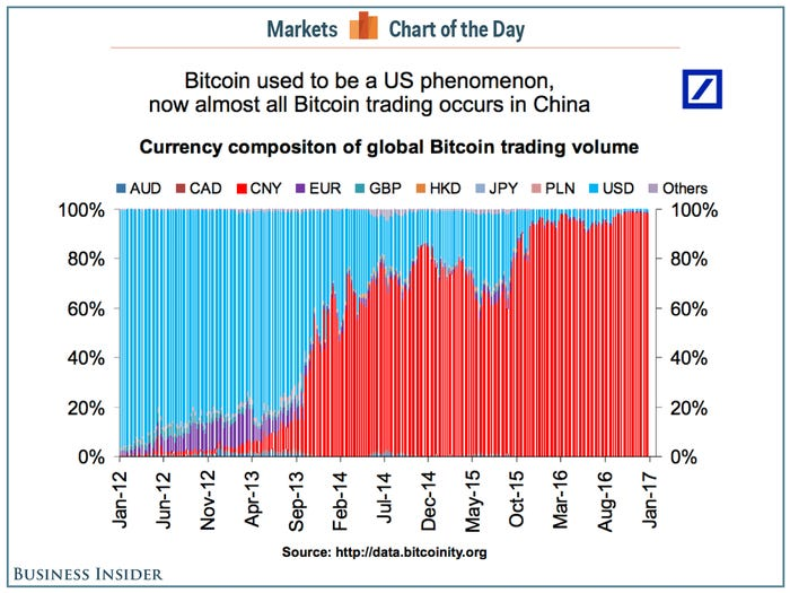

Most of the world’s largest cryptocurrency exchanges were also founded in China, like BTCC, Huobi, OKCoin, and KuCoin. Huobi and BTCC would both go on to become the world’s leading exchanges by volume over the coming years, catering to Chinese and international demand for Bitcoin. Goldman Sachs issued a report in 2015 highlighting that 80% of bitcoin trades were paired against the Chinese yuan, saying:

Thus far, most merchant Bitcoin activity has been concentrated among US and European-based merchants. Despite China’s higher trading activity, restrictions enacted by the PBoC to limit Chinese Bitcoin companies’ access to traditional Chinese payment processors have prompted many large Chinese companies to stop accepting Bitcoin. However, in light of a somewhat stabilizing Bitcoin economy in China, a few payment processors have reemerged, such as BTC China’s JustPay.

These companies continued to cater to the demand from Chinese investors looking to Bitcoin for speculative gains and perhaps to avoid the strict capital controls in China. By 2016, the BTC/yuan pair reportedly accounted for 90% of the total BTC trading volume.

2016–2017: ICOs Boom and The Chinese Government Bans Bitcoin (Again)

Chinese demand for Bitcoin continued to grow in 2016, with China holding fast as the main participant in Bitcoin trading. Major financial institutions began to express an interest in Bitcoin, and a report issued by Deutsche Bank revealed the massive role China was playing in Bitcoin network activity.

In 2016, the Huobi exchange’s total volume surpassed $250 billion, accounting for over 60% of all global Bitcoin activity. Bitcoin’s price rallied 120% to $952 that year, and many new cryptocurrencies launched with varying degrees of success. 2017 saw the rise of initial coin offerings (ICOs), a new method of fundraising destined for controversy. Investors bought new crypto tokens using Bitcoin in the hopes that the tokens would increase in value. The whole process essentially mirrored that of securities sales, with one difference: Bitcoin and other cryptocurrencies were not considered legal tender and not yet explicitly regulated in China.

That changed in late 2017. Chinese ICOs raised over $400 million earlier in the year, prompting the Chinese government to ban ICOs entirely on September 4. A second measure was put in place on September 17, prohibiting all Chinese crypto exchanges from trading. This was essentially a ban on Bitcoin itself, issued from the country responsible for the majority of crypto trading; at the same time, the crypto market dipped 6%, potentially in response to this news. Hundreds of cryptocurrency exchanges would be shut down or relocated following the new regulations. While Chinese traders couldn’t buy locally, they still had access to international exchanges, and the Chinese market continued to grow despite the crackdown.

Chinese mining pools continued to account for most of the hashrate, with four of the five largest pools in 2017 based in China.

Although trading was becoming more regulated, Bitcoin continued to be minted and traded in China more than any other country in the world.

2019: China Praises Bitcoin vis-à-vis Blockchain, Preps State Crypto for Launch

In November 2019, the Chinese state media surprised readers by releasing a front-page report praising Bitcoin as a successful application of blockchain technology. This report was issued a month after President Xi Jinping made statements supporting blockchain technology, saying that China should look to blockchain as a way to further its economic development.

The statement may herald a significant influx of funding entering the Chinese blockchain sector. Most Chinese blockchain VCs left the market following the 2018 crash, and now, it seems, the government may be attempting to reignite the industry’s development. Three Chinese firms have already set up a $1 billion blockchain investment fund since the press release. In the few hours following the president’s remarks, the price of Bitcoin surged from $7,500 to over $10,000.

It’s clear that China is a major influence on Bitcoin. The Chinese government has taken a keen interest in the project, one way or another, for years. In fact, the central bank of China has developed its own form of digital currency to be released in the coming months. To date, state cryptocurrencies have been met with widespread skepticism and poor adoption. However, as the largest bank in the world in a country with close ties to its major companies, the People’s Bank of China may be uniquely positioned to distribute a state-run crypto on a wider scale than we’ve ever seen.

Unlike Bitcoin, the digital yuan will be fully centralized, under the control of the Chinese authorities. Where Bitcoin was originally invented as a means to circumvent fiat currency, the digital yuan will strengthen it, allowing the yuan to be easily spent anywhere in the world. How the release of the Chinese government’s crypto will impact Bitcoin — or, indeed, the fiat currencies of other nations — remains to be seen.

Bitcoin and China in 2020

Bitcoin’s journey has been closely linked with China since it first reached state media attention. The nation is a hub of blockchain investment, BTC trading, and Bitcoin mining. The timeline of Bitcoin’s development in China highlights the power that a single government can have over the price action of the world’s leading cryptocurrency.

At the moment, the market volatility that stems from Chinese press releases on Bitcoin is still significant. However, the network continues to grow. As Bitcoin continues to see widespread, mainstream adoption throughout the world, we could see a reduction in China’s influence on Bitcoin in 2020.

The above references an opinion and is for informational purposes only. It is not intended as and does not constitute investment advice, and is not an offer to buy or sell or a solicitation of an offer to buy or sell any cryptocurrency, security, product, service or investment. Seek a duly licensed professional for investment advice. The information provided here or in any communication containing a link to this site is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject SFOX, Inc. or its affiliates to any registration requirement within such jurisdiction or country. Neither the information, nor any opinion contained in this site constitutes a solicitation or offer by SFOX, Inc. or its affiliates to buy or sell any cryptocurrencies, securities, futures, options or other financial instruments or provide any investment advice or service.