If you think that the Bitcoin network is at the mercy of its miners, you’re wrong.

If you think that it’s at the mercy of its developers, or its users, you’re wrong, too.

These sorts of polemic stances that accuse one group of having total authority over Bitcoin are all too common in casual conversations and established news sources alike. When we focus on the undue influences of a single faction of the Bitcoin community, we lose sight of the broader picture: the picture of a community where checks and balances incentivize these groups to stay together rather than splitting apart.

Here’s a look at the mutually reinforcing relationships between miners, developers, and users in the Bitcoin community. We’ll look at them in three regards: (1) what function the group serves in the community, (2) what existential threat this group could pose to the broader community, and (3) what incentives work to mitigate this threat.

⛏️ Miners

The tireless builders of the blockchain are the miners: individuals and pools of people who use their computing power to add new blocks to the blockchain, verifying new transactions and bringing new coins into circulation in the process. When Satoshi Nakamoto first put forward the idea of Bitcoin, just he and a few other people mined BTC; now, entire fields of computers are dedicated to this task.

Miners’ function: creating and securing the chain

The mining of Bitcoin is what makes it possible for the blockchain to be decentralized and secure. By verifying transactions and preventing the network from being hijacked, miners do the work of making sure that Bitcoin is able to function as a plausible store of value at all. If people were able to illicitly spend the same money more than once, then Bitcoin wouldn’t be viable as a cryptocurrency — but the miners’ majoritarian confirmation of transactions prevents this from happening.

The threat of miners: mining a different cryptocurrency

The problem is that there are now countless cryptocurrencies in circulation, and miners can choose to mine virtually any of them. And if enough of them decide to move off of Bitcoin and start mining something different — if another blockchain were more profitable to mine, for example — Bitcoin could be critically compromised: it could take a very long time for transactions to be added to the blockchain and validated, which would end up making BTC impractical to use for just about anything.

In practice, some cryptocurrencies (like Ethereum) have different hashing algorithms and are therefore difficult for Bitcoin miners using ASICs (application-specific integrated circuits) to spontaneously start mining instead of Bitcoin. That’s because ASICs are built to operate only on one specific hashing algorithm in order to be as efficient as possible.

However, other cryptocurrencies — most notably, Bitcoin Cash — do use the same hashing algorithm, which has historically led to BTC miners oscillating between mining BTC and BCH depending on which is more profitable at any given moment. This is one of the reasons why some Bitcoin Cash detractors are so negative towards that newer cryptocurrency: it takes miners’ attention and resources away from Bitcoin.

How this threat is mitigated: a critical mass of users

What keeps miners sticking around rather than leaving and posing an existential threat to Bitcoin? In large part, the users.

Miners follow the profit, which is a function of four factors:

- the reward for mining a new block

- the difficulty in earning the reward

- the cost of running the mining rigs

- the blockchain’s transaction volume

In the long run, transaction volume should lead the way here: as more people are actively transacting with a cryptocurrency, its value (and, therefore, its price) increases, which means that both the mining fees and mining rewards become more valuable.

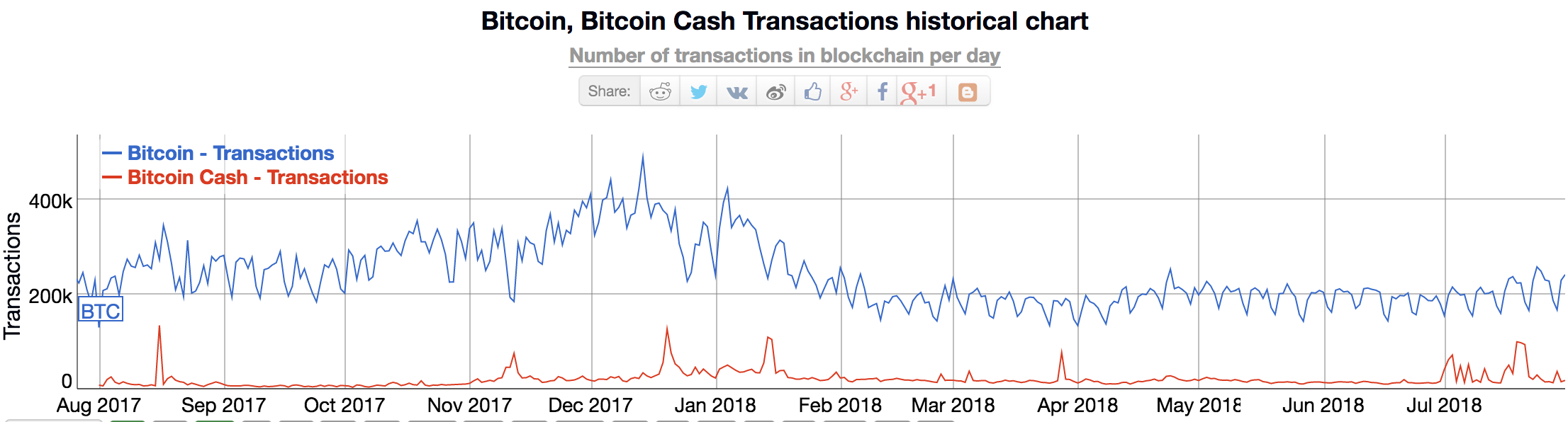

Bitcoin has a huge number of transactions that need to be processed at any given time. To continue comparing BTC with BCH, take a look at this chart contrasting their transaction volumes:

Bitcoin’s transaction volume has consistently been an order of magnitude greater than Bitcoin Cash’s — and with all of those transactions to process, there’s no reason for miners to collectively jump ship in the long run. With smaller cryptocurrencies, it’s possible that interest will eventually die down and miners will jump ship — but given the fact that Bitcoin still has ~50% overall market dominance, it’s plausible to suppose that, at least for the foreseeable future, it has a critical mass of users and transactions that will keep miners invested in securing the chain.

💻 Developers

While miners are continuing to propagate and secure the blockchain, developers are working to enhance the efficiency and functionality of the Bitcoin protocol across all dimensions. Bitcoin’s status as an open-source project gives a diverse range of people the power to contribute to its burgeoning ecosystem.

Developers’ function: improving bitcoin’s functionality

You don’t hear about Bitcoin developers in the same way that you hear about Ethereum developers because they aren’t working on diverse, unusual DApp projects. Instead, they’re all working on one thing: improving the basic functionality of Bitcoin as a protocol for storing and transferring value.

Bitcoin developers focus on improving every aspect of Bitcoin: its security, its transaction speed, its scalability, and so on. For instance, one of the highest-profile Bitcoin development projects, Lightning Network, aims to make Bitcoin transactions faster and cheaper by developing a network for settling many transactions off of the Bitcoin blockchain proper. Projects like this keep Bitcoin constantly improving to better serve (and invite more people into) its ecosystem.

The threat of developers: starting off-chain projects

Ethereum isn’t just a different animal than Bitcoin: to some people, it’s also symbolic of the greatest existential threat to Bitcoin’s ecosystem. That threat is developers deciding to create their own blockchain to underpin their new project, rather than building that project on top of Bitcoin.

Why didn’t Vitalik Buterin and the other minds behind Ethereum decide to create their own blockchain rather than staying on Bitcoin’s blockchain? There are many possible answers, but one particularly cynical answer still has a lot of people worried about Bitcoin’s ecosystem: it was more profitable to launch the project as its own cryptocurrency than it was to build it on top of Bitcoin.

University of Cambridge research fellow Garrick Hileman had this to say about developers migrating away from Bitcoin:

Very talented people who are coming into the space now may have more of an incentive to try to build their own cryptocurrency or new blockchain-based system rather than to build on something that’s already in place because we’ve seen [from projects like Ethereum] that you can create something new and you can accrue tremendous value if you are on the ground floor of that.

A brand-new crypto project can be difficult to get off of the ground — but if it does get traction, its developer can capture “tremendous value”:

- Ether initially cost about $3 USD and now costs about $420 USD (140 times its original value)

- Litecoin initially cost about $4 USD and now costs about $77 USD (over 19 times its initial value)

- XRP initially cost about $0.0046 USD and now costs about $0.43 USD (over 93 times its initial value)

When you build something on top of an established blockchain whose value has already been priced, it can be hard to capture the astronomical value that gives the space its allure for so many people. On the other hand, if you can build something from the ground up and get people interested, it might seem more possible to have this kind of outsized success — even though most crypto projects don’t have anywhere near the success of something like Ethereum.

How this threat is mitigated: mutually assured destruction

It’s important to note that this threat to the Bitcoin blockchain may not be entirely mitigated yet: many blockchain developers do still seem to be setting off to make their own projects, whether that’s a totally new project or something built on top of Ethereum. One way it could be mitigated in the medium term, though, is through the notion of “mutually assured destruction”: the idea that if the crypto space fragments too much, especially early on in its development, it risks snuffing itself out.

As we discussed above in reference to miners, so much of a blockchain’s value and success depends on it achieving a critical mass of users actually using it. While we’re still trying to convince the world at large of blockchain’s value, it’s important to have a blockchain project sufficiently large that it demonstrates the sheer scale at which this technology can and should operate. High-profile, high-transaction-volume projects like Bitcoin are part of what proves that blockchain is a compelling concept rather than a slew of small-scale schemes reminiscent of the dot-com era. It’s that image which helps to attract the attention of industry outsiders, and that image is threatened when projects splinter off of Bitcoin.

👩 Users

Ultimately, Bitcoin is something for people to use, whether they use it as a currency, a store of value, a speculative instrument, or something else entirely. Miners and developers put in the work for the sake of these end-users.

Users’ function: making the network valuable

“If you build it, they will come” — but, if they don’t come, it doesn’t matter how great that thing you built is.

The presence of people who are actually using Bitcoin to store value, buy things, and sell things is what makes it compelling. Think of it like the internet: if all of the worldwide web’s infrastructure were in place but no one actually created websites or services for it, the web would just be an idle tool. It might still have the same potential that it has today, but it certainly wouldn’t have the same actual value.

This is why widespread adoption of Bitcoin is so important: mass use of the cryptocurrency is what turns it from Monopoly money into real money. Back in 2010, even though Bitcoin had much of the same infrastructure that it has today, you couldn’t buy much of anything with it because it was so new and so few people were actually able to transact with it — it famously took two bold, super early adopters of Bitcoin and 10,000 BTC (currently valued at $75,379,200 USD) to buy two pizzas from Papa John’s. Now, Bitcoin is more valuable because more people understand its functionality and accept it as payment — but it still has a long way to go if it wants to be as ubiquitous as cash or gold.

The threat of users: churn from the network

Bitcoin is a little like Tinkerbell: it’s gained momentum as people have come to believe in it, but if people abandon it, it’ll lose all that value once again.

The most fundamental danger to Bitcoin’s ecosystem is that people will stop using it. There are multiple risks that could encourage this kind of churn:

- Maybe people lose faith that Bitcoin has a unique value proposition beyond that of fiat currency or gold.

- Maybe governments decide to majorly crack down on digital currencies such as Bitcoin.

- Maybe other crypto projects will gradually siphon core users away from Bitcoin.

Right now, there’s reason to be optimistic that these possibilities won’t come to pass — but every one of them, unlikely though they may be, poses an existential threat to the network.

How this threat is mitigated: clear value propositions

There are two pillars within the community that work to mitigate this existential threat, and the developers and companies within the Bitcoin space are responsible for upholding them:

- education.

- easy user experience.

If we only talk about Bitcoin in jargon like “decentralized ledger” and “off-chain scalability,” no one who isn’t already inside of the industry will suddenly start caring about Bitcoin. We need to talk in plain and compelling language about what makes Bitcoin valuable if we want it to see truly ubiquitous adoption. That’s Pillar #1: education.

Then, once people decide to take a chance on entering the Bitcoin ecosystem, their experience as a user needs to be intuitive and simple from Day 1 onwards. People wouldn’t live online if they needed to understand CSS and HTML to use a website; just so, even if people understand Bitcoin’s basic value proposition, they probably won’t use it if they find themselves burdened with overly technical interfaces. This is Pillar #2: easy user experience.

Put simply, Bitcoin is ultimately a product, and it needs smart product design to win in the long run: people have to understand why they need it, and they have to find it dead-simple to use.

Bitcoin’s success depends on respect for checks and balances

We’ve seen that each of Bitcoins three core communities play a key role in holding the overall ecosystem together:

- Miners keep the blockchain secure and growing so there’s something for developers to improve and end-users to use.

- Developers improve the efficiency and user experience of the protocol so that it’s something users actually want to use.

- Users spend and hold Bitcoin as a means of value transfer and storage, making BTC sufficiently valuable that miners want to commit resources to mining it.

If you want to understand the value proposition of Bitcoin, you need to understand this delicate balance: no one group has totalitarian authority over the others.

When people stop believing in societal norms and cease to respect the institutions on which government is founded, constitutional crises happen. States reject the authority of the courts; the legislature rejects the validity of the executive; very quickly, the checks and balances that kept society smoothly running begin to fragment.

When we fail to see the full Bitcoin ecosystem and argue over the primacy of miners or the influence of developers, we set ourselves up for the same kind of crisis. Let’s start by acknowledging that every stakeholder in the Bitcoin community matters, and move forward — together — from there.

The above references an opinion and is for informational purposes only. It is not intended as and does not constitute investment advice, and is not an offer to buy or sell or a solicitation of an offer to buy or sell any cryptocurrency, security, product, service or investment. Seek a duly licensed professional for investment advice. The information provided here or in any communication containing a link to this site is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject SFOX, Inc. or its affiliates to any registration requirement within such jurisdiction or country. Neither the information, nor any opinion contained in this site constitutes a solicitation or offer by SFOX, Inc. or its affiliates to buy or sell any cryptocurrencies, securities, futures, options or other financial instruments or provide any investment advice or service.